|

Understanding through Discussion |

|

|

Register | Sign In |

|

QuickSearch

| EvC Forum active members: 64 (9164 total) |

|

| |

| ChatGPT | |

| Total: 916,823 Year: 4,080/9,624 Month: 951/974 Week: 278/286 Day: 39/46 Hour: 1/3 |

| Thread ▼ Details |

|

Thread Info

|

|

|

| Author | Topic: Tax Talk | |||||||||||||||||||||||||||||||||||||||

|

dwise1 Member  Posts: 5950 Joined: Member Rating: 5.1 |

Let's compare our experiences with taxes under the new tax laws. Or is it still too soon?

First, we need to think about the metrics that we use. We've been hearing a lot of complaining about smaller or negative refunds (ie, they end up having to pay more than was withheld). Most of that is because of what I call "Bush 41 'Tax Cut' Effect". Remember when G.H.W. Bush gave us a "tax cut" which did not actually cut our taxes, but rather artificially reduced the amount of withholding from our paycheck? While that gave us a little more cash each pay period, in the end we still owed the same amount in taxes and ended up with either lower refunds or not having had enough withheld and having to pay out-of-pocket. IOW, the exact same thing we're seeing people hit with now and for the same reason. Many people plan for that refund and have even already spent it, so having it reduced or eliminated is hitting them hard. That means that changes in your refund is not the right metric to use. Instead, the real metric should be whether the actual tax amount has changed and in which direction. Not only would that entail comparisons of actual tax rates, but also the effects of changes in deductions. From the IRS website you can download a PDF with the tax tables (plus all forms and instructions). If you are a wonk, you can compare the tax tables from 2017 and 2018 and work out all the changes in tax brackets, tax rates, etc. Or you could simply compare both years' taxes if your financial situation was mostly the same. My financial situation changed drastically from 2017 to 2018 because I retired, which makes that comparison more difficult for me. Instead, I took my 2017 taxable income and tax owed and looked it up in the 2018 tax table:

A 2.38% tax cut doesn't seem like much to crow about to me. Does it to you? We have a new higher standard deduction, but is it truly higher? Last year, we had both a personal exemption and a standard deduction, but this year exemptions have been eliminated, it appears that the old personal exemption and standard deduction have been combined into the "new higher" standard deduction. Let's look at the numbers so that we can do the math (my basic approach to several YEC claims):

So instead of nearly doubling your standard deduction (as I seem to recall they tried to sell it to the public), they simply rolled your personal exemption into it and give you a measly little increase. Another consideration with the new standard deduction is how it compares with what you used to be able to deduct through Schedule A itemization. For example, this year my itemized deductions were greater than the new standard deduction, so I lost that $4050 personal exemption amount and I ended up paying more taxes on that amount -- sure, it was just $24 more this year in my new lower bracket, but it was more nonetheless. A tax cut is supposed to mean paying less in taxes, not more. And what about the exemptions for dependents? That's also gone now and is covered instead by "Child tax credit/credit for other dependents" on line 12a. It is calculated on Form 2441, which is a standardly byzantine flow-charty tax form. It also employs a fraction multiplier which depends on your income (from .35 for the lowest income graduating up to .20 for $43000 and above). I'll have to leave it to how it worked out for someone with dependents, who will hopefully report whether they had gained or lost on that change. While you're crunching your own numbers, keep in mind that for a meaningful comparison your finances had to have remained about the same. For example, if your income and deductions were close to the same between 2017 and 2018, then you can make a meaningful comparison. If not (like me by having retired), then you need to compensate. What about the rest of you? Any unpleasant surprises? Any pleasant ones?

|

|||||||||||||||||||||||||||||||||||||||

|

dwise1 Member Posts: 5950 Joined: Member Rating: 5.1 |

In the OP, I mentioned what I call the "Bush 41 'Tax Cut' Effect" in which they claim to have given you a "tax cut" when in reality all they did was to reduce your federal tax withholding, giving you a little bit more take-home pay every pay period, while keeping your actual taxes the same, giving you a very nasty surprise come tax time. Which is what many people are experiencing and complaining about now.

This morning my phone's news feed presented a USA Today article, Another tax headache ahead: IRS is changing paycheck withholdings and it'll be a doozy, which reports that there's a new W-4 form being rolled out to correct Trump's version of the "Bush 41 'Tax Cut' Effect". The article describes how filling out the new W-4 is like filling out your 1040, plus it raises privacy concerns as it ends up containing a lot of personal info that your employer will have to keep on file and hopefully protect as per HR PII (personally identifying information) requirements. Since exemptions no longer exist (see the OP, Message 1), you have to enter all your other taxable income (eg, from your second and third jobs), including from your spouse's job(s), and all your deductions, etc. Every employer will need to provide non-trivial training for all their employees to be able figure out how to fill out the new form. The result of all that pain is supposed to be a much more accurate withholding rate which will result in withholding that just barely covers your taxes, such that it will pay for your taxes with near-zero refund. While that is the ideal level of withholding, most people have gotten used to using withholding as a kind of "Christmas Club" savings account and depend on that sudden "bonus" in their budget planning. Except for all the pain, the new form will address a long-standing problem with the old (current) W-4 form based solely on exemptions (now no longer in existence) and which underestimated withholding for two-paycheck families, such as what mine was. For example, I have been estimating my next year's taxes for a couple decades because the old W-4 was woefully inadequate. We were a two-income family with my then-wife ending up making slightly more than I did. One year we owed a lot because too little was withheld. If that were to happen again, then the IRS would fine me for under-withholding, so to prevent that I estimated the next year's taxes, estimated the withholding shortfall, and had that much extra withheld from my pay -- that is how I spotted the "Bush 41 'Tax Cut' Effect". And I have continued that practice with an Excel spreadsheet that I wrote for that purpose.

|

|||||||||||||||||||||||||||||||||||||||

|

dwise1 Member Posts: 5950 Joined: Member Rating: 5.1 |

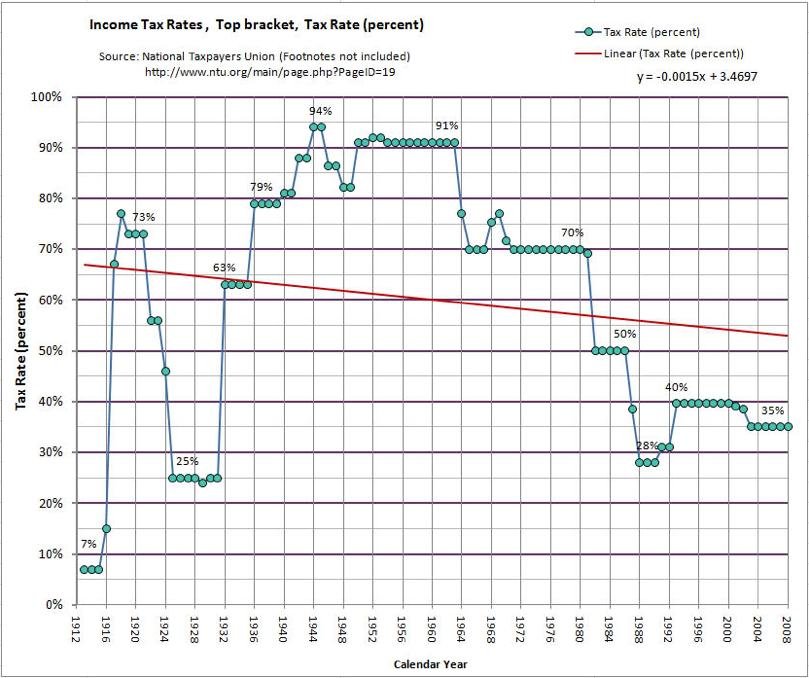

Our current tax brackets stop at $500,000 for singles or $600,000 if filing jointly. With a Federal rate at that point of 37%. Would it be that difficult to create some additional ones? Something like: $500,000 - $1 million : 39%$1 million - $2 million: 41% $2 million - $4 million: 43% $4 million+ : 45% This could be tweaked, but is this really that hard a sell? It won't change the tax rates of the vast majority of people. It would be a hard sell for the rich who crave ever more money and they are the ones who own the Republicans. Speaking of MAGA {grin}, the mythical time in the past when America was great appears to have been the 1950's when we were building our infrastructure and our industry led the world. What enabled that was:

Here is a chart of the top income tax rates over time:

And this tired old canard of Republicans saying it would hurt small business owners. I call BS. Virtually all businesses are LLCs of some sort. They are taxed differently. This only affects a person's individual income.

Yes, BS for the reason that you give. But small businesses are still being hurt by the tax system while large businesses thrive. Elizabeth Warren presented a flat corporate tax, 7% on all corporate profits over $100 million (eg, Elizabeth Warren’s new plan to make sure Amazon (and other big companies) pays corporate tax, explained: No more claiming big profits to investors while paying nothing to the IRS). Large corporations end up with huge profits and pay no taxes (or even get large refunds) because they can afford armies of lobbyists and armies of tax lawyers, whereas small business who cannot afford those armies are left to bear the brunt of business taxes. This weakens the economy even more, because small businesses are the primary job creators. We saw that in the 2008 crash when small businesses were forced out of business by banks refusing to give them standard short-term loans which caused unemployment to soar.

|

|||||||||||||||||||||||||||||||||||||||

|

dwise1 Member Posts: 5950 Joined: Member Rating: 5.1 |

My effective tax rate dropped from 22.03% in 2017 to 19.94% in 2018. So a drop of 2.09%. Not huge from a percentage standpoint, but a decent amount considering my income which usually hovers around $200,000. Mind you I am already in a pretty low cost area, living in Central Florida. One thing I'm curious about is deductions. I assume that your itemized deductions are greater than the new "and improved" standard deduction of $12,000 (you said you have no dependents, which I assume also means that you file as single). That would mean that, like me, you completely lost out on that $4050 deduction we used to have as a personal exemption but has been rolled into the new standard deduction (IOW, they really gave us hardly anything with the tax scam law). How did that impact you? I'm retired now with these sources of income:

Federal income tax views Social Security benefits as non-taxable, but only up to a point which I go past. In addition, any other form of income makes even more of your Social Security income taxable, so about $4000 of my Social Security ends up being taxable -- this year that figure was $9000 because I retired in mid-January so I received pre-retirement income for the first two weeks of the year. I did get a refund. Estimating for next year, withholding from my military pension will very nearly match my federal tax, so I should get a refund of about $11. California state income tax does not tax Social Security benefits. It also still has personal exemptions. As a result, my state income tax was less than zero, so effectively zero and I got all my withholding back as a refund. The same will happen next year. However, the year I turn 70½ I will need to start withdrawing about $18,000 each year from my IRAs. That will count as additional income and will make a bit more than $18,000 of my Social Security taxable -- in effect, my taxable income will increase by about twice my IRA disbursement. My estimated tax will increase from $700 to $3700. My state tax will be less than $100, but still no longer zero.

|

|||||||||||||||||||||||||||||||||||||||

|

dwise1 Member Posts: 5950 Joined: Member Rating: 5.1

|

My perspective is filing as Single, so your perspective of filing as Married Joint allows us to examine the effects on that. Modifying my table in the OP, Message 1, slightly:

Assuming home ownership and hence property taxes, a household's itemized deductions should not be twice as much for Married Joint than it is for Single. That should make it more likely for a Single's itemized deductions to exceed the Standard Deduction than for Married Joint. However, except for a measly extra $3200 more leeway this year, you should have been able to do better taking the standard deduction in past years and hence your past taxes should have been just as easy as you found them this year. Remember, a large part of that new standard deduction comes from you having lost the exemptions for you and your spouse. If you didn't use to have to itemize (taking that small $3200 increase into account), then you ended up losing the deduction game.Now to use your remark as a springboard, I see your few brief comments and raise the issue you mention: If the Trump tax cuts hadn't included huge breaks for the rich and for corporations that caused a huge increase in the deficit that Trump wants to pay for by cutting programs like Social Security then I would think it a big win. Cutting Social Security benefits would have no effect on the deficit. Social Security benefits are funded entirely from a special trust fund that is separate from the part of the budget that creates the deficit and therefore is not connected to the deficit and has no effect on the deficit. That trust fund is funded by special payroll taxes listed on pay statements either as "Social Security" or "FICA" (Federal Insurance Contribution Act). No other tax revenue sources are used, which isolates it from what's really creating the deficit. The issue of Social Security running out of money is because of changing age demographics. In the past there were more workers than beneficiaries so that trust fund grew and was invested wisely in gov't bonds. Now the baby-boomers are retiring and drawing benefits so we now are having more beneficiaries and fewer paying into the system. There are several possible solutions, one of which is to cut benefits, but note that such cuts would still have no effect on the deficit. Medicare Part A (Inpatient/hospitalization) is funded similarly with FICA payroll deductions going into a special Medicare trust fund, separate from the part of the budget that creates the deficit, which completely pays for Part A benefits. Medicare Part B (outpatient) is a straight-forward medical insurance program funded entirely by insurance premiums paid monthly by all beneficiaries -- it's not even part of the budget and so has no effect on the deficit. Medicare Part C (supplemental and advantage policies) and Part D (pharmaceuticals) are private medical insurance policies, which obviously have nothing whatsoever to do with what's really causing the deficit. Social Security and Medicare have nothing to do with the deficit -- not so with Medicaid, but that program is very much smaller. Slashing Social Security or Medicare benefits would have absolutely no effect on the deficit. GOP plans to use such slashing to reduce the deficit that they have caused are nothing but BS lies! Stepping down from my soapbox now.

|

|||||||||||||||||||||||||||||||||||||||

|

dwise1 Member Posts: 5950 Joined: Member Rating: 5.1 |

Property taxes in NH are high so in the past we did better itemizing. Before we paid off the mortgage we did even better itemizing. Well, I'm Southern California, so I don't know how we compare in terms of property tax. Instead of us getting into compare sizes, let's just call it close enough to a draw. Glad to hear that you've paid off your mortgage. For many years it had been a goal to pay off my mortgage before retiring, so I'm glad I achieved that. I cannot imagine trying to retire with a mortgage payment or rent hanging over my head (in my neighborhood, the amounts of the two are not that much different).

bout Social Security, Medicare and Medicaid, I won't guess at the details of how Trump and the Republicans plan to raid these programs to decrease the annual deficit, but my understanding is that that is what they want to do. For example see Senate Republicans Set Sights On Cutting Social Security and Top Republicans are already talking about cutting Medicare and Social Security next. I quickly read through both stories, but could not see any mention of how cutting Social Security or Medicare was supposed to have any effect on the deficit, only that the GOP (Greedy Old Pricks) wanted to slash those programs using the deficit as an excuse. Is there anybody who can make an actual case of reducing the deficit by slashing Social Security or Medicare? Certainly Faith is their most vociferous shill here, but I cannot see how even she could be so willfully stupid to make such a case (though I do not doubt that I could be surprised).

|

|||||||||||||||||||||||||||||||||||||||

|

dwise1 Member Posts: 5950 Joined: Member Rating: 5.1 |

Percy writes:

The money was used to purchase treasury bonds, which brought a return in the form of interest payments. Treasury Bonds were a good investment (since inflation was knocked out by the time of the 1983 law). Reagan signed a law that raised social security taxes that somehow transferred the increased income into the general fund (Ronald Reagan and The Great Social Security Heist). If it could be done once it could be done again. And treasury bonds were purchased, by Social Security, long before Reagan, and ever since. (Do you prefer investing Social Security surplus funds in the Stock Market?) Very true! For decades I had heard rumors of the federal government having systematically "stolen" funds from Social Security. Finally a couple years ago I learned what that was about and it is as you describe. Social Security benefits are paid from from payroll taxes created for that purpose. Surplus taxes go into a trust fund which is managed by trustees. Those trustees are required to invest that surplus wisely. Normally, the wisest investments are in government bonds, so that is what they have bought. That clearly appears to be the basis of all those rumors I had heard growing up. BTW, the Medicare Trust Fund for managing Medicare Part A (In-patient) is managed in the same manner -- Part B (Out-patient) is funded by insurance premiums paid by participants (the $144 that Part C commercials promise to refund you from your Social Security check) and Parts C (supplemental and Advantage programs that are being massively advertised on TV right now) & D (prescriptions, often included in Part C policies) are both private medical insurance. BTW, here is the YouTube posted by the OLLI program at Cal-State, Fullerton, of this year's annual "Transitions in Retirement" (TIR) Social Security presentation. If it is the same as the one I attended a couple years ago, it explains not only how Social Security benefits are calculated, but also how the program is funded. That includes how the trustees of the Social Security Trust Fund are required to invest surpluses wisely, which basically involves buying government bonds.

It was that OLLI TIR presentation that clued me in on how massively the GOP is lying about Social Security and Medicare (next Saturday's TIR presentation via ZOOM, YouTube video to be posted around 06 Nov -- these on-line accommodations made necessary by the pandemic and the fact that OLLI members are high-risk (seniors)) causing our massive deficit. Entirely different money pots involved. The only effect on the deficit is the government's debt on those bonds that the trust funds have bought. "The more learning, the more life!" (Pirke Avoth, "Sayings of the Fathers")

|

|||||||||||||||||||||||||||||||||||||||

|

dwise1 Member Posts: 5950 Joined: Member Rating: 5.1 |

I find that Trump is pulling that same old deceptive trick as Bush 41 did.

In the OP, I mentioned what I call the "Bush 41 'Tax Cut' Effect" in which they claim to have given you a "tax cut" when in reality all they did was to reduce your federal tax withholding, giving you a little bit more take-home pay every pay period, while keeping your actual taxes the same, giving you a very nasty surprise come tax time. Trump's "payroll tax deferment" BS is almost exactly the same as the nonsense that Bush 41 (AKA, "G.H.W. Bush", "Bush Senior", "Bush I") had pulled, only much more pernicious and greedy. What Bush 41 did was to curry favor with the people by putting a little more cash in their pockets now, deceptively calling it a "tax break" (whenever you hear a Republican say "tax break" or "tax cut", run for your life!), whereas in reality he was just feeding them dribbles of the income tax return that they were still expecting to receive and budgeted for and were surprised to find wasn't there in the end. But, like everything else Trump ever does, Trump's "elimination of the payroll tax" really only benefits him and corporations. Everyone who still receives a paycheck and is not a member of government and school district workers exempt from Social Security, please look at your paystub. You should see an entry in either two forms: either FICA (Federal Insurance Contributions Act tax) which I had seen for decades, or see it broken down as Social Security and Medicare as in my last job. They are supposed to amount to 7.65% of your income and they go into the Social Security and Medicare trust funds to fund those programs. But, at the same time your company must match your FICA contributions for a total contribution of 15.3%. Despite all necessary norms, Trump is still fully aware of what businesses he's running and what effects taxes have on them (among many other opportunities for outright corruption, but, à la Irma la Douce (1963), "that is another story" ("Das ist eine andre Geschichte." *NOTE). For a business with many employees, they see a lot of money going out to payroll taxes, so if they could just get rid of those payroll taxes then they'd have a lot of money, even millions of dollars, to play with. So of course those business men (and losers like Trump) would want to see payroll taxes go away. Which of course is why Trump is so hot and heavy on getting rid of payroll taxes. Screw the people! Just give me my tax break! As it is, all Trump was able to do was to defer payroll taxes until the end of the year. So who could ever benefit from that? Well, if you are a worker who suddenly has an extra $80 per paycheck (a nominal figure I have heard) then you will use that to pay off your debts or buy what you have needed but could not afford. But then at the end of the year, you will suddenly be getting paid $80 per paycheck less to make up for those deferred payroll taxes -- "deferred" means "deferred", duh? So you are now much further behind than you were before. Whom will you blame? Good Santa versus Bad Santa. It's an old Republican game. The GOP plays "good Santa" in order to completely screw up the economy in order to leave a complete mess for the Democrats to clean up, thus forcing them into the role of "Bad Santa". OK, so part of deferring payroll taxes is Trump's promise to make that deferment permanent. Of course, that will kill Social Security and Medicare, but what does Trump care just so long as it gets rid of the payroll taxes? In the meantime, as some businesses have played along with that payroll tax deferment, that leaves so many of their workers vulnerable to financial difficulties as they could not afford to put any of that extra money aside, but had to spend it to take care of pressing necessities. Now after the election they are facing a situation of grave financial difficulty. A pundit has stated that those workers are now being extorted to vote for Trump since he will make those deferments permanent whereas Biden will not. But making those deferments permanent will mean the death of Social Security and Medicare. {BEGIN NOTE *:

In the 1963 US comedy, Irma la Douce (1963), Lou Jacobi plays the bartender breaking the fourth wall to provide commentary to the audience. In doing so, he always starts to allude to far greater adventures that he had engaged in only to suddenly break it off by saying, "Das ist aber eine andre Geschichte.", "But that is another story."

END NOTE}

My personal problem with this movie is that I have only ever seen it dubbed into German. For example in the introduction, I still have no idea what the original English line was for "Aber man lebt nicht von Kohl allein." as the camera focuses in onto the cabbage in the morning market before cutting to the working girls. It doesn't make sense in colloquial English even though it was for an American English-speaking audience. In American English we do have the expression that one does not live on bread alone, but there was no bread in sight. In American slang, both "bread" and "lettuce" refers to money as does cabbage ("Kohl") refer to money in German slang (eg, in a 70's comedy film where the rent money had been accidentally buried until the furnace's coal and then later re-discovered, "Ich have den Kohl unter den Kohlen gefunden!" ("I found the money (cabbage) under the coals!")). Then it turns out that the movie's director, Billy Wilder, was from Germany and had been building his career in the Weimar Republic before defecting to the US in 1933. Was that his German leaking through in that intro shot?

|

|||||||||||||||||||||||||||||||||||||||

|

dwise1 Member Posts: 5950 Joined: Member Rating: 5.1

|

As you may recall, when the GOP Congress created the Great Tax Scam of 2017, while the rich got the greatest share in the form of permanent cuts, the poor not only got very little in terms of cuts, but those cuts were also temporary. Those cuts start to go away next year for everybody making less that $100,000 a year and the poor's and middle classes' (AKA, "the nouveaux pauvres") taxes will start to rise.

As per this Ring of Fire video, Republicans Rigged The Tax Bill To Raise Working Class Taxes After The Election, the GOP plan was to time those increases to after this election. If there'd be a new President (the situation we do have), then the GOP would blame the new administration for those tax increases even though it was the GOP who put them in place. And if Trump had been reelected, then they'd say "Oh dear! Well we have to remedy this with yet another massive tax cut favoring the rich and tossing table scraps to the poor again!"

Here are the video notes:

quote: And here's a transcript:

quote: A truly devious and dastardly twist to the GOP's standard game of "Good Santa, Bad Santa." Edited by dwise1, : Slight grammatical correction (to maintain parallelism) in my writing

|

|||||||||||||||||||||||||||||||||||||||

|

|

Do Nothing Button

Copyright 2001-2023 by EvC Forum, All Rights Reserved

![]() ™ Version 4.2

™ Version 4.2

Innovative software from Qwixotic © 2024